You must have heard a lot about CareShield Life these recent months, and if you’re confused, you have come to the right place. Here is a very comprehensive guide about CareShield Life, broken up into an easy-to-digest format for you. You can also easily extract information from each individual portion if you like.

ElderShield To Be Replaced By CareShield Life

CareShield Life is basically an upgraded version of ElderShield, a basic insurance scheme to cater for your long-term care needs in the event of severe disability, especially in old age. Introduced in 2002, those born in 1979 or earlier have the option to opt-out of this scheme.

To provide better support for Singapore citizens and permanent residents who become severely disabled during their old age, Prime Minister Lee Hsien Loong announced the review of ElderShield in 2016. As a result, CareShield Life which will expand the role of insurance, was created.

ElderShield was replaced by CareShield Life in 2020, and it will no longer be available to new cohorts turning 40 from 2020 onwards. However, it will continue to operate for existing cohorts who are already enrolled if you choose to continue your ElderShield plan.

What Is CareShield Life?

Health Minister Gan Kim Yong said that 1 in 2 Singaporeans who is healthy at age 65 is expected to be severely disabled at some point in their lifetime and require long-term care. Severe disability may arise due to a sudden disabling event (e.g. stroke and spinal cord injuries), the worsening of chronic conditions and diseases (e.g. diabetes), or the progression of illnesses as we age (e.g. dementia).

Launched on 1 October 2020, and similar to ElderShield, CareShield Life is also a long-term care insurance scheme that provides basic financial support and long-term care costs should Singaporeans become severely disabled, especially during old age, and need personal and medical care for a prolonged duration (i.e. long-term care).

Here is more information about the new insurance scheme for Singaporeans.

Activities of Daily Living (ADLs)

How do we define severe disability, or differentiate it from moderate disability? It is defined as the need for assistance in at least three out of these Activities of Daily Living (ADLs):

- Eating

- Getting dressed

- Using the toilet

- Bathing

- Moving

- Walking around

- Getting from the bed to a chair, or vice versa

Will You Be Covered By CareShield Life?

Singapore Citizens or Permanent Residents born on or before 1979:

If you are born on or before 1979 (aged 41 and above in 2020), participation is optional (except foreigners who become Singapore Citizens or Permanent Residents from 1 Oct 2020 onwards and are not born in 1979 or earlier. It is compulsory as long as you are not severely disabled). Your current ElderShield will continue to cover you if you are enrolled in one, or you can also choose to join the new scheme from end-2021 if you are not severely disabled.

To make it more convenient for you, if you are born between 1970 and 1979 (aged 41 – 50 in 2020), insured under ElderShield 400, and not severely disabled, you will be automatically enrolled into CareShield Life from end-2021. But you can opt out by 21 Dec 2023 if you do not wish to remain on the new scheme. More information will be provided then.

Singapore Citizens or Permanent Residents born after 1990:

If you are born after 1990 (aged below 30 years old in 2020), you will automatically be covered when you turn 30, regardless of regardless of pre-existing medical conditions and pre-existing disabilities. You will receive a letter about two months before you turn 30, and closer to your 30th birthday, you will start paying the premiums.

Singapore Citizens or Permanent Residents born between 1980 to 1990:

If you are born between 1980 to 1990 (aged 30 – 40 years old in 2 020), you will automatically be opted into CareShield Life on 1 Oct 2020, or when you turn 30, whichever is later and regardless of pre-existing medical conditions and disability. Do look out for a letter between September to October last year with your policy details.

Singapore Citizens or Permanent Residents born after 1990:

If you are born later than 1990, you will automatically be opted-in when you turn 30.

CareShield Life Premiums

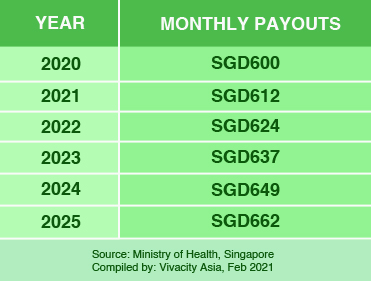

Similar to ElderShield, CareShield Life offers a payout when you have severe disability, to help finance the hefty cost of your long-term care. You will receive lifetime cash payouts as long as you remain severely disabled, with the payouts increasing overtime – starting from SGD600 per month in 2020. You will be covered for life once all premium payments are completed by age 67. Payable in full via MediSave, there are Government subsidies available if you need help with the premiums.

Premiums for the new scheme begin from age 30 to 67 years of age, starting at SGD206 for male and SGD253 for female, starting at age 30 for both. Annual premiums will increase at a 2% rate for the first five years, but this rate of increase will be decided again by the CareShield Life Council. From 2026 onwards, an independent CareShield Life Council will review the premium adjustments regularly based on factors such as the claim experience, changes in life expectancy, and disability trends.

If you already have a severe disability at the joining age of 30, you will need to only pay the first premium to qualify for lifetime payouts. If you’re eligible for a payout, you will stop paying premiums even if you are younger than the last premium payment age of 67 years.

You can check your personalised premiums here.

Government Subsidies

Singaporeans will receive up to SGD250 over the first five years to help them pay for the premiums of CareShield Life. If you have a monthly per capita household income of less than SGD2,600, you are eligible for additional subsidies. Check out more information on the government’s CareShield Life website.

Medisave Care

Medisave Care is a supplement scheme that provides financial aid to Singaporeans aged 30 years and above, who are Medisave Care, launched on 1 October 2020, is a long-term care supplement scheme that provides financial aid to Singapore citizens or permanent residents aged 30 years and above, who are afflicted with severe disability, by providing cash support of up to SGD200 monthly from their Medisave accounts. However, you must have a minimum balance of SGD5,000 in Medisave to ensure premiums for MediShield Life, hospitalisations and other critical medical costs are still covered. You are also allowed to tap into your spouse’s Medisave account if you do not have enough to qualify for Medisave Care.

If you meet the eligibility criteria, you can submit an application to the Agency for Integrated Care (AIC), a government-accredited severe disability assessor.

Estimated Monthly Payouts

Even when CareShield Life’s payout increases in the future, once you start to collect your payout, this amount will be fixed and will not increase. The payout amount will be fixed at the amount the year you pay the last premium at age 67.

How do you make a CareShield Life claim?

You can’t simply claim that you’re unable toIf you are unable to perform 3 out of 6 ADLs, you need to undertake a severe disability assessment and be officially assessed by an MOH-accredited severe disability assessor before you can make a successful claim.

The cost of an assessment is SGD100 at a clinic and SGD250 if the assessor goes to your home, although this fee is waived if it is your first assessment. The full assessment fee will be reimbursed with your first payout if you are found to be severely disabled. Once you have been assessed as severely disabled, you can submit a claim application form to the Agency for Integrated Care (AIC). If you have a private CareShield Life supplement plan, you may contact your agent to make a successful claim.

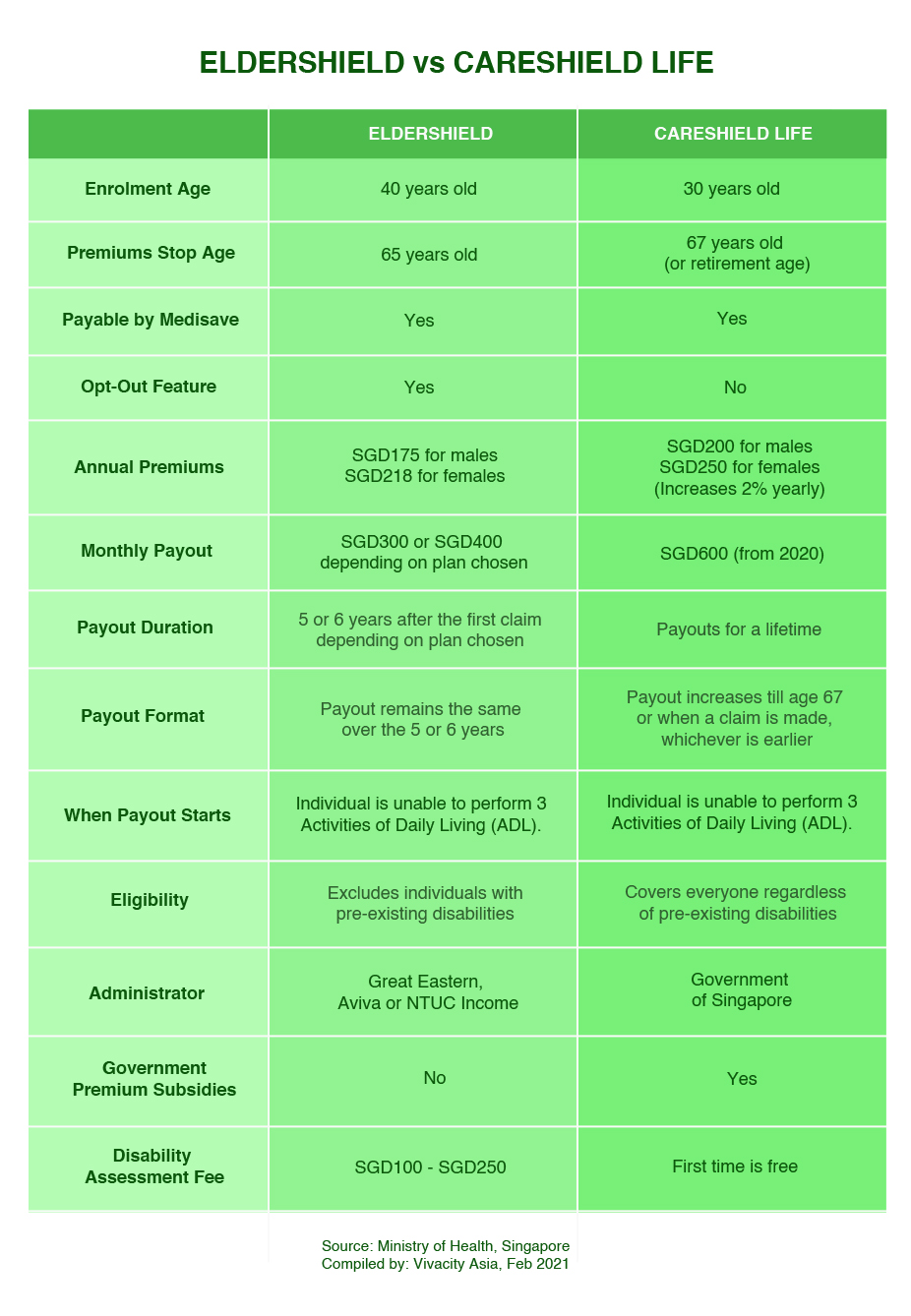

Differences Between ElderShield and CareShield Life

There are many key differences between ElderShield and CareShield Life, although both schemes are designed to help Singaporeans and Permanent Residents cope with the cost of long-term disability.

One of the key differences between CareShield Life and ElderShield is the former’s lower enrolment age of 30, compared to the latter’s age of 40. CareShield Life is also compulsory for all individuals born in 1980 or later, as opposed to ElderShield’s opt-out feature. On 1 October 2020, all Singapore residents between 30 to 40 years old will start paying premiums and be included in CareShield Life. As for disability payouts, ElderShield provided SGD300 per month for 5 years (or SGD400 per month for 6 years, for ElderShield 400), while with CareShield Life, you can receive SGD600 per month from the start, with the payouts increasing overtime, for life. All the differences are documented in our comparison table below.

Can I Switch from ElderShield to CareShield Life?

If you’re born after 1980 and want to remain insured by ElderShield, you can opt-out of CareShield Life by 31 December 2023. If you’re born in 1979 or earlier, you are not automatically opted into CareShield Life, but you can opt-in if you wish, from this year. If you have opted out of ElderShield but want to opt-in for CareShield Life, you can do so as long as you are not currently disabled.

Can You Enhance Your CareShield Life?

CareShield Life offers just a lifetime payout of just SGD600 in 2020 in the event of a severe disability, but according to a research carried out by the National University of Singapore, Singaporeans aged 65 and above who are living alone would need at least SGD1,379 per month for basic needs, which put you at a deficit should you become severely disabled. As such, it is highly recommended for you to enhance your CareShield Life with supplementary plans that can be purchased from private insurers, such as GREAT CareShield from Great Eastern Life. You can also supplement this with other long-term care insurance plans if you have additional budget. (Get in touch with us at hello@vivacityasia.com if you want to know more.)

Source: CareShield Life, Ministry of Health Singapore https://www.careshieldlife.gov.sg/

Looking for more financial planning content? Here are some resources that you can check out:

Working Up to Retirement Age Shortens Your Years

Aging In Singapore – Kids Are No Longer Your ‘Insurance’

Confused about CareShield Life? Not Sure If It’s Right for You?

You’re not alone — many people have questions about how CareShield Life works and how it fits into their long-term care plan. Whether you’re new to it or just need some clarity, we’re here to help! Our Singapore-based financial advisers (10+ years of experience) will break it down in simple terms and help you make informed decisions.

Got questions? Reach out to us at hello@vivacityasia.com — we’ll guide you through it step by step.